[ad_1]

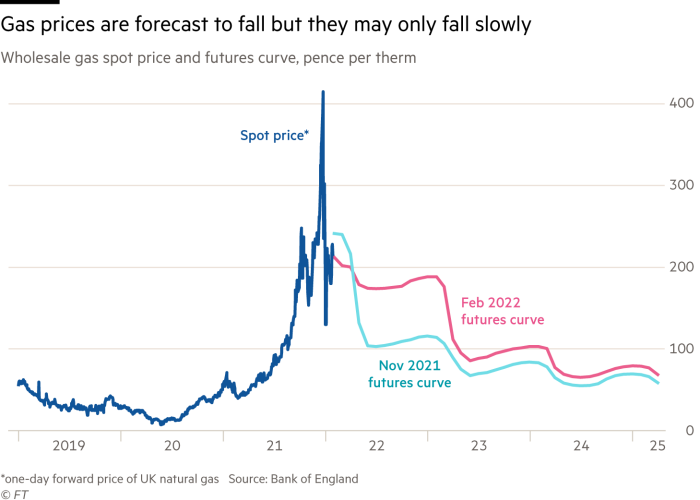

The Bank of England is forecasting the weakest growth of real post-tax labour incomes in more than 70 years, with a fall of 2 per cent this year and a further half a per cent in 2023. This depressing outlook captures the challenges generated by sharply higher import prices and the risks of more generalised inflation. Among leading high-income economies, the UK seems to be particularly hard hit. Inflationary risks seem similar to those in the US. But the UK is also a large net importer of energy, especially gas, as prices have exploded upwards. The government might have hoped that the fading of the pandemic’s clouds would leave a sunlit economy. But, as is their wont, events got in the way. The economy, the people and the government face hard times .

The Bank’s Monetary Policy Reportout last week, noted: “Global inflationary pressures have continued to build significantly, largely driven by the sharp increases in energy prices and upward impact of the imbalance between supply of and demand for tradeable goods on their prices. On a UK-weighted basis , four-quarter world export price inflation, including energy, is expected to have risen to around 11 per cent in 2021 Q4.” The UK cannot take back control from the world economy. Remarkably, the US alone generated almost all of the increase in consumption of goods among the group of seven leading economies last year. That then drove the supply bottlenecks.

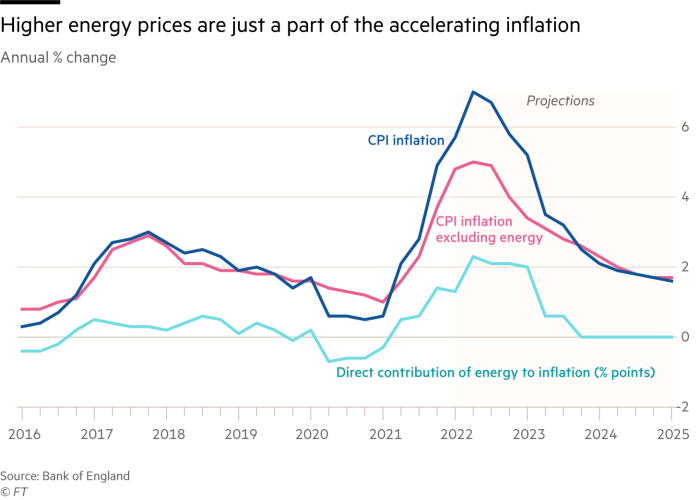

The Bank forecasts peak inflation at 7¼ per cent in April, with three-quarters of the increase between last December and April being due to rising energy and goods prices. But it has a still bigger problem, which is similar to that of the US. The labour market is running hot. Unemployment is already below its equilibrium rate, the Bank believes. Less speculatively, companies report recruitment difficulties and high vacancies. On balance, concludes the report, there is excess demand in the economy, which is not yet the situation in the eurozone.

What makes the situation more difficult is that higher prices of imports, especially energy, impose an overall economic loss. As we learned in the 1970s, such losses must be absorbed. If people play a game of pass the parcel, by insisting on higher wages and salaries in order to offset the reduced real incomes, the outcomes would either be a squeeze on profits, which would damage investment, or cause an inflationary spiral, which would damage almost everybody.

Andrew Bailey, the BoE governor, duly remarked last week that “we do need to see a moderation of wage rises . . . in order to get through this problem more quickly.” This remark was certainly unpopular and probably useless. But analytically he was right. The more wage earners seek to restore their purchasing power in an economy hit by these externally imposed losses, the higher will be inflation and the more merciless the needed monetary squeeze. Boris Johnson’s desire for a high-wage, high-growth economy is irrelevant. The worry is that the monetary policy needed to curb second-round inflationary risks will end up even more economically damaging than the Bank and indeed almost anybody else now thinks.

Yet this is not just about monetary policy. Just as in the US, though in different ways, fiscal policy is also relevant. This is so in two distinct ways. One is that only the government has the means to cushion the badly hit against the losses imposed by higher prices, especially of energy. The second and broader dimension is that the overall fiscal stance will bear on overall demand and so influence what the Bank needs to do.

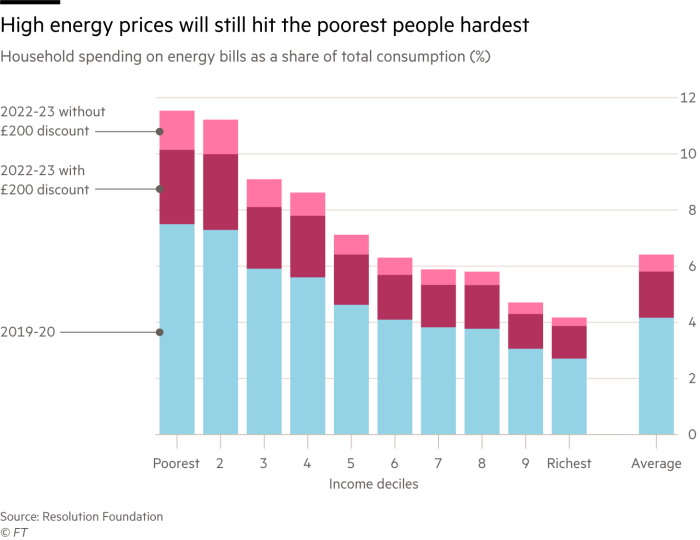

On the former, the government has introduced a broad package of measuresconcentrated on alleviating rising energy costs, with £9bn (0.4 per cent of gross domestic product) spent next year. The measures consist of a £200 discount on all electricity bills from October, which would cost £5.5bn. Yet this is to last just a year and subsequently must be repaid. If energy prices remain high, many people are likely to struggle and even fall deeply into debt. A further £150 of support will go to households in the bottom four council tax bands, at a cost of £3.5bn. According to the Resolution Foundationeven after the £200 rebate, the annualised increase in energy prices (after the jump in the price cap in April) will be 39 per cent.

This package is ill targeted. Much of the benefit will go to people who do not need the money and significant numbers of poorer people will fail to receive it, partly because council tax is out of date, being based on the 1991 value of properties. Overall, the burden on the poor will still remain the heaviest because they spend the highest proportion of their incomes on energy. (See charts).

Meanwhile, the planned increase in national insurance contributions, supposedly to pay for additional spending on health and social care, is set to go ahead. I have argued before that both the tax itself and the social care policy it finances are indefensible. As important today is the fact that this increase in taxation will be added to the impact of higher prices of energy and other goods and services. An optimist might argue that this combination of hits to demand will at least allow monetary tightening to be significantly smaller than it would otherwise have needed to be. A pessimist might respond that such a multiple whammy will make workers even more determined to recoup their lost real incomes via higher wages.

High inflation, sharp rises in energy costs and a weakening economy are now with us. The foolish tax rise on the way will make it worse. The Bank forecasts growth of 1¼ per cent next year and 1 per cent in 2024. The government hoped for better. No such luck. Unhappy times are here again.

[ad_2]

Source link