[ad_1]

CalPERS is singlehandedly making a case against government by doing precisely what libertarians allege: abusing their control of public funds by overpaying themselves for shoddy work.

As we will explain in more detail, CalPERS’ new compensation consultant, Global Governance Advisors, is enabling the giant pension fund’s staff in misappropriating from beneficiaries via the device of fundamentally and pervasively flawed pay benchmarking. The biggest fail is benchmarking CalPERS against private fund managers, without making adjustments for the considerable benefits that CalPERS employees get by working for a public pension fund, the biggest being that it’s virtually impossible to fire them once they get past probation. The second is not recognizing and allowing for the fact that the sort of fund management that CalPERS is doing is not high-skill active management, but lower-skilled running of index funds (which let us be clear actually does take skill) and choosing third-party fund managers…with the assistance of consultants…begging the question of the value added by CalPERS employees.

The third serious lapse is not acknowledging the elephant in the room, that CalPERS is underperforming even peer and considerably smaller public pension funds. Since CalPERS has low turnover and adverse selection bias (the underperformers have every reason to stay since they can’t be fired and they won’t be called to account at CalPERS), the effect of this or any scheme that benchmarks off private fund managers will be to pay even more for underperformance.

We’ve embedded a key slide shows to be presented at the CalPERS board meeting this Tuesday at the end of this post. You can view the full agenda here.

Global Governance Advisors Fails to Call Out Serious Flaws in Current Bonus Scheme

What is particularly disappointing is that Global Governance Advisors is new to CalPERS and was perceived to be less staff-friendly than their predecessor. That is not how things appear to be shaking out in practice. In fairness, Global Governance Advisors may feel it can only make changes at the margin to existing practices; see how the consultant simply edits the Compensation Policy for Executive and Investment Management Positions document.

For instance, Global Governance Advisors is not willing to challenge CalPERS current absurd bonus framework. From their opinion letter:

The current metrics used within the Annual Incentive program were first introduced as part of a new annual incentive plan for the 2016-2017 fiscal year with shared organizational metrics that aligned awards for all positions to the following performance areas:

• Fund Performance (both Total Fund and Asset-Class based)

• Enterprise Operational Effectiveness

• Investment Office CEM Results

• Customer Service

• Stakeholder Engagement…While the metrics have generally worked for CalPERS….

“Generally worked for CalPERS”? If one means to serve as a cover for overpaying staff and thus currying loyalty to Marcie Frost, yes, but those results are completely contrary to CalPERS’ fiduciary duties to its beneficiaries.

The lame excuse for paying all staff for results in areas that had nothing to do with them was to foster everyone working together. But first, there was no evidence of pre-existing lack of cooperation that needed to be addressed. And if that were a problem, that’s the sort of thing the top brass are supposed to fix, rather than use it as an excuse for wallet-fattening.

Second, to underscore the ludicrousness of the current approach, three of the six metrics are based on Investment Office activities (the “CEM results” is benchmarking on costs). The Investment Office, including all of its related analytics and compliance activities, consists of less than 20% of total staffing at CalPERS. It is hard to fathom how or why functions that have nothing to do with that, like pension and health insurance processing and customer service, should get bonuses based on whether the Investment Office overspends. .

One might argue that these other departments should also not be affected by Investment Office non-performance, but guess what? CalPERS already pays performance bonuses even in the event of underperformance. No, I am not making this up. It’s worse than the common practice of giving children prizes for merely showing up. These are the payout levels for the Total Fund performance benchmark, based on the last five years’ results:

Note staffers get 76.3% of the bonus award if they merely meet the benchmark? So this is tantamount to getting paid an incentive award for merely doing your job. And they still get a bonus even if they fall short of the benchmark by as much as 15 basis points!

CalPERS Has Performed Badly…Yet You’d Never Know From Bonus Metrics

The consultant Global Governance Advisors, despite its name, seems unaware of or uninterested in how CalPERS has been performing of late, since that ought to inform how it thinks about pay and bonuses.

CalPERS latest fiscal year investment performance was abysmal. CalPERS was at the bottom of the pack among public pension funds. This is utterly disgraceful because its huge size means it at least ought to do better on costs, which will improve performance, and its large and supposedly professional staff ought to be able to achieve superior returns.

The fact that CalPERS is so grossly underperforming other public pension funds, including its Sacramento sister CalSTRS, says its problem is not pay, since mere public pension funds with smaller and less well paid staffs are cleaning its clock, investment-wise. Highlights from our August post CalPERS Comes Dead Last of 34 Public Pension Returns Despite Having Biggest, Best Paid Investment Office:

Despite having the most heavily staffed and luxuriously paid investment office of any public pension fund, CalPERS scored the worst investment returns of any of 34 funds tracked by Pensions & Investments.

As you can see at the Pensions & Investments site, CalPERS return for fiscal year 2020-2021 was 21.3%. The next lowest was tiny Kern County, more than two and a half points higher, at 23.9%. CalPERS’ Sacramento sister CalSTRS delivered 27.8%. The stars were Texas County, at 33.7&. New York Common, at 33.6%. San Bernardino County, at 33.3%, Oklahoma Teachers, at 33%, and Oklahoma Firefighters at 31.8%. Mississippi PERS came it at 32.7%, but that was gross of fees. Nevertheless, five funds earned a full 10% in investment returns more than CalPERS, and the pension fund arguably the most similar to CalPERS in terms of scale did more that 6% better.

That extreme laggard result also fell short of CalPERS benchmark of 21.7%. Recall that investment expert Richard Ennis explained at length that public pension funds and their consultants devise their own benchmarks, and they not surprisingly wind up being unduly forgiving

An earlier paper by Ennis found that even though nearly all public pension funds generated negative alpha, as in they actively destroyed value, CalPERS was one of the worst, coming in at number 43 out of 46, with a stunning negative alpha of 2.4%. From a 2020 post:

Ennis’ conclusions are damning. Both the pension funds and the endowments generated negative alpha, meaning their investment programs destroyed value compared to purely passive investing.

Educational endowments did even worse than public pension funds due to their higher commitment level to “alternative” investments like private equity and real estate. Ennis explains that these types of investments merely resulted in “overdiversification.” Since 2009, they have become so highly correlated with stock and bond markets that they have not added value to investment portfolios. From a 2020 post:

Alternative investments ceased to be diversifiers in the 2000s and have become a significant drag on institutional fund performance. Public pension funds underperformed passive investment by 1.0% a year over a recent decade…

CalPERS is a standout in the “negative value added” category, ranking 43 out of 46, with a “negative alpha” of 2.36%. This is a particularly appalling scoring, since CalPERS has far and away the largest and best paid investment office of any US public pension fund. But is this outcome partly result of CalPERS paying its investment team for merely showing up? The investment office staff perversely receives performance bonuses for merely almost hitting their benchmarks, which means achieving what CalPERS has defined as “market” performance. As we’ll discuss soon, Ennis describes how those benchmarks are self-serving and more favorable than using simple, broad stock and bond market proxies.

You will never hear any honest account from CalPERS about how dreadful its performance was. The giant fund is trying to present its back of the pack performance as some sort of actual, as opposed to perverse, accomplishment, by pointing to the fact that it finally beat its 7% performance target. So too did virtually everyone in America who didn’t put their money in a mattress.

Back to the current post.

CalPERS games its performance benchmarks. We’ll return to the point mentioned in our 2020 post cited above, that CalPERS, like most public pension funds, games its benchmarks. Recall it has an overall return target which it uses to project long-term returns. That means it serves as the basis for projecting income and thus determining how much to charge the many employers that contribute to CalPERS in the current year.

CalPERS also has benchmarks within its various strategies, so it has a private equity benchmark, a public equities benchmark, a fixed income benchmark. But CalPERS and other public pension funds get to do what private sector fund managers cannot do because they are in a competitive market: pick benchmarks that are too easy to hit, a as opposed to ones that reflect investible strategies that are alternatives to what you are doing. Oh, and another luxury public pension investment managers allow themselves: changing their benchmark formula just because (bonuses).

Here’s recent corroboration of CalPERS’ benchmark too cuteness, from Mitch Bollinger:

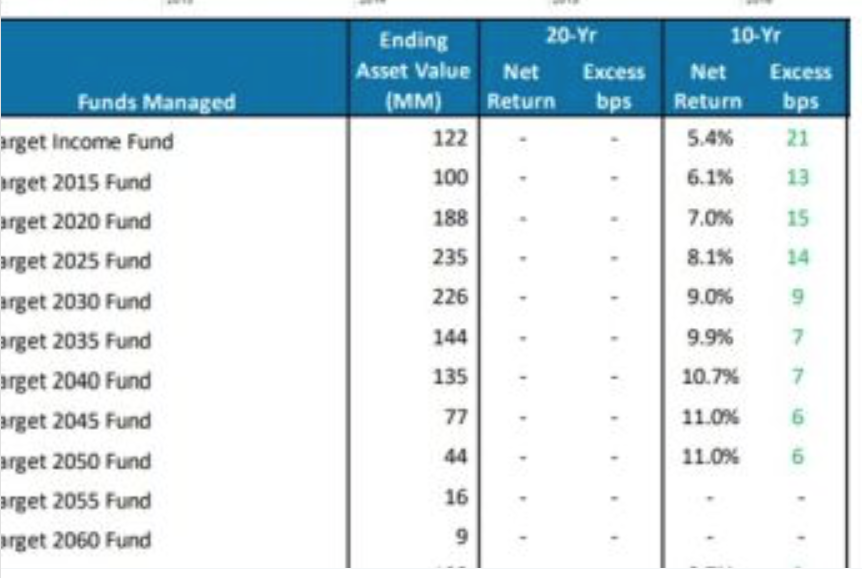

Further analyzing CALPERS’ performance report linked below, CALPERS runs a series of target date funds for their supplemental income plans. If we compare the performance of the TDFs CALPERS runs in these plans to Vanguard’s low fee TDFs with similar target dates, we see very consistent nominal underperformance of around 1% annually.

Yet if you look at how CALPERS reports the performance of these funds, we see that they show consistent outperformance of their benchmark in the neighborhood of 10 bp. It appears the key to benchmark outperformance is less about getting good returns and more about picking a poor performing benchmark.

Yves again. So as you can see from the table, CalPERS claimed it outperformed in target date funds on a ten year return basis…each and every measurement period (!) when it’s actually been wildly underperforming.

Gaming private equity benchmarks is pervasive. Oxford professor Ludovic Phalippou has discussed this process from time to time. It was once widespread for both academics studying private equity and many investors to use a simple benchmark of the S&P 500 plus 300 basis points. There wasn’t an evidence-based justification for a 300 basis point hurdle; it was just a rough and ready way to acknowledge that private equity is riskier than common stocks, both by virtue of the use of leverage and its illiquidity. But the use of the S&P 500 as the basis for comparison was clearly flattering, at least from the 1990s to the mid 2010s. The average size of an S&P 500 member was vastly larger than a typical private equity firm, and so those private equity buys would show faster growth and hence higher average returns.

CalPERS for years had fallen short even of its house private equity benchmark (which did not use the S&P 500 but more exotic indexes), for pretty much every time period except for 20 years when it was still picking up some of the “glory years” period of 1995 to 1999. Then it fixed that problem by changing both the stock reference to one widely regarded as more forgiving…..and lowering the risk premium from 300 basis points to 150.

CalPERS will continue to perform badly. In case you thought last year’s terrible results were an anomaly, think again. This year, CalPERS will have write-downs on its 301 Capitol Mall “hole in the ground” project, its $900 million in Russia holdings. Former Chief Investment Officer Ben Meng increased CalPERS’ Chinese holdings, but the Shanghai composite is down nearly 8% over the past year, while the S&P 500 is up over 5%.

These dogs are indicative of CalPERS and other big fund’s problems: they are following a fundamentally failed approach. In an important article where renown investment analyst Richard Ennis explained that their overdiversification is hurting performance:

Trustees of public pension funds and large endowments in the U.S. are in a bind. With the help of staff, consultants, asset managers, assorted pundits and a media chorus, they have rationalized the division of their portfolios into as many as a dozen different sub-portfolios, commonly known as asset classes. Additionally, they behave as if they believe they can beat the market with 100 or more asset managers, which they compensate to the tune of 1-2% of the value of their assets each year. None of this is working for them, and certainly it is not working for the stakeholders of these funds. Ennis (2020) found that public pension funds collectively have underperformed passive investment by 1.0% per year and large endowments by 1.6% per year. It is time for fiduciaries to recognize that they have not merely been unlucky. Rather, their strategy has failed them.

Global Governance Advisors Seeks to Pay Even More For Non-Performance by Amping Up Fundamentally Flawed Approach

Most of the Program Principles document below is devoted to cleaning up inconsistencies and making small improvements and is therefore not controversial. But there is one section, which admittedly Global Governance Advisors largely inherited, that needs to be called out:

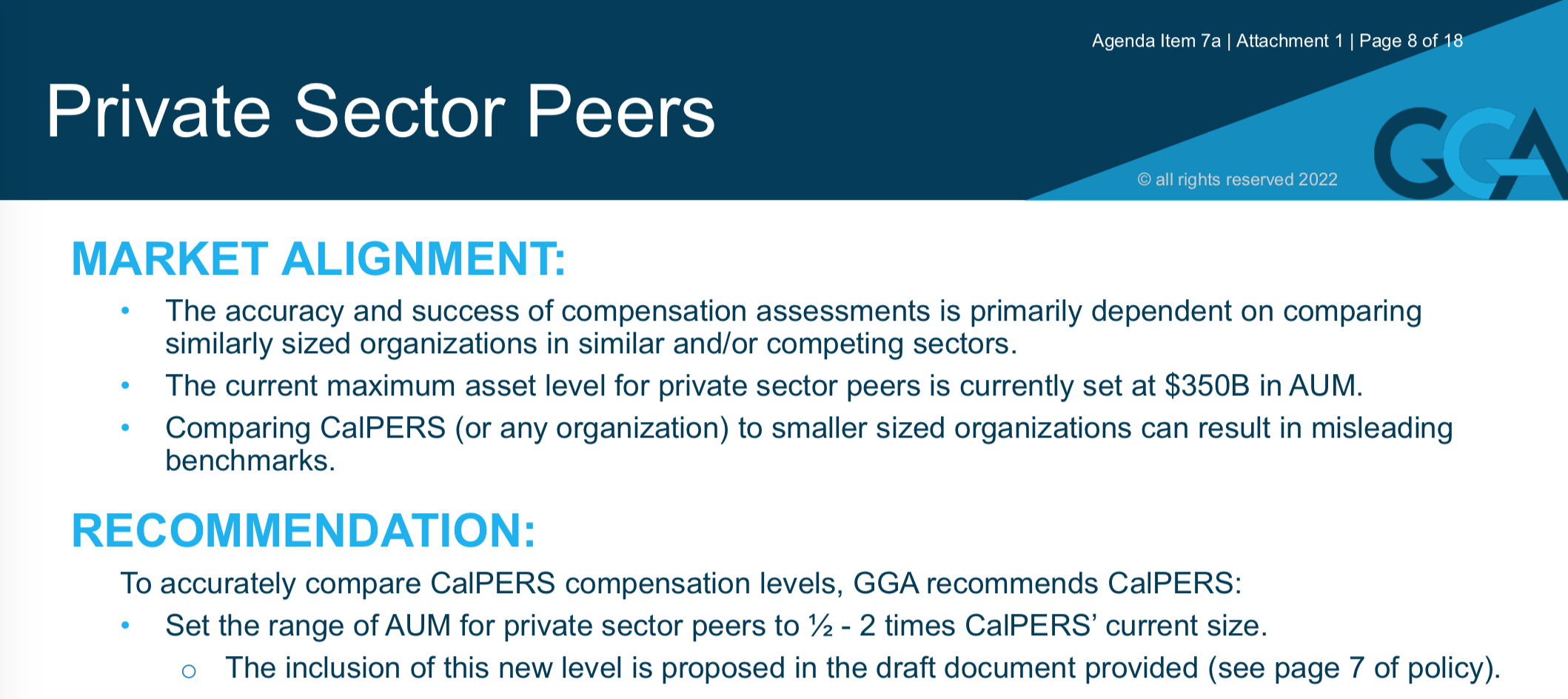

Simple-minded benchmarking of CalPERS against private sector fund managers for pay and personnel practices is utterly misguided. Working for CalPERS is an extremely low risk proposition and comp levels need to be lower accordingly. Private sector pay levels need to be adjusted down for the following:

The de facto job guarantee at CalPERS. Once a staff member has gotten past the probation period, it is virtually impossible to fire them. Former Chief Investment Officer Ben Meng made that clear. Via e-mail from a former investment office staffer:

The best story I heard from the investment office was when Ben addressed them at the quarterly all staff meeting. He stood up in front of the whole office pointed his finger at them and said you should all be lucky to have a job. If we were in the private sector you would all be fired because of how bad the performance numbers are.

Let’s look at the CalPERS poster child of value destruction and failing upwards: Dan Bienvenue, now the Deputy Chief Investment Officer. Bienvenue made an enormous emerging markets value bet that in 2017 cost Global Equities billions. In early 2017 the emerging markets bet was working. But then it went badly south and Bienvenue could not unwind his bet. The wager was so large and the underperformance so great that it resulted in negative performance to the total fund. That meant Bienvenue’s losses hit everyone in the Investment Office’s bonuses, with the most senior suffering the biggest opportunity cost. The outcome included a lot of screaming and swearing and then an internal investigation.

The scuttlebutt from former Investment Office employees is the head of the performance group questioned whether there was a complete lack of controls in the Global Equities group, to the degree that the performance group recommended that all strategy implementation cease. As a result, most of the active strategy funds were closed. As one former Investment Office professional said, “The true downside was how badly Dan destroyed both fund value and culture within the Investment Office”

The fact that what most large private funds do is different from, as in harder than, what CalPERS does. Under Ben Meng, CalPERS got rid of most of its in-house actively managed funds. CalPERS is largely an indexer. Most of its other investment activities consist of selecting external managers. That requires a ton less acumen and entails much less risk and stress than running money yourself.

To give a very incomplete idea of the magnitude of external versus internal action, if you simply increasing the private equity carried interest reported in the 2020 Comprehensive Annual Financial Report by the 21-22 fee increase percentage, Real estate and private equity fees and carried interest can be conservatively projected at $1.25 billion, against a budget of under $700 million for everything else CalPERS does. The 21-22 budget proposal was misleading — at best.

The value of the pension. Very few private sector financial services firms offer pensions (beyond C-suite deferred comp schemes). When McKinsey was recruiting in the 1980s, it had a very elaborate pension scheme whose contributions were worth an additional >12% in current pay. The failure to allow for that in the CalPERS pay comparisons is glaring.

The value of the very generous health benefits. This would not amount to as large an adjustment as the pension benefits.

Global Governance Advisors winds up admitting to the inconsistency of its, or perhaps more accurately CalPERS’ position that Global Governance Advisors isn’t willing to buck. Despite invoking the oxymoron of “Private Sector Peers,” the opinion letter we cited earlier in this post has Global Governance Advisors making approving noises about current incentive metrics based on “Typical Performance Metrics Observed in the Pension Fund Industry,‘ as in other government pension funds.

Mind you, that isn’t to say that CalPERS shouldn’t also look at what private fund managers are doing. but that means making apples to apples comparisons, not naive and misguided sized based ones. CalPERS should look primarily at indexers and should strip out its private equity and real estate portfolios in making any size comparisons. And since CalPERS is allegedly thinking about bringing private equity in house, it should make a separate study for that team only.

But again, the offending bit is that Global Governance Advisors is about to update CalPERS private sector comp list based largely on the rising tide of increasing asset values, with no consideration whatsoever to the fact that Ben Meng considerably de-skilled the Investment Office, and the comp selection should reflect the much narrower expertise now deployed.

In other words, the “private sector peers” part of the exercise is very likely to boost pay, when CalPERS industry-topping compensation is delivering bottom of the barrel results. There should be pay freezes for all executive and investment office positions until CalPERS gets to the bottom of why it is doing so badly with the most lavishly paid and heavily staffed investment team.

Sadly, multiple former employees and other insiders point to the same cause: no one who is very good would want to work for Marcie Frost or Dan Bienvenue. Both are perceived as unwilling to have anyone around them who might outshine them. Frost recently playing Chief Investment Officer in trying to ‘splain how CalPERS will deal with inflation is one of many examples of her overestimation of her competence. So if CalPERS were to attract anyone who was well qualified, they’d be stymied or would stay long enough to get their ticket punched and move on.

Now admittedly, solving the underlying problems are beyond Global Governance Advisors mandate, but it would be nice if they demonstrated some recognition of what was amiss at CalPERS and attempted some mild prods in the right direction. Even though the consultant is reporting to the board, it probably feels it has been hired by the problem, as in Frost and her cronies among the staff.

[ad_2]

Source link