[ad_1]

After months of debate, the Federal Reserve plans to shrink its $9 trillion balance sheet in an attempt to tighten monetary policy and tackle the highest inflation in decades.

detail Elements of the plan were included in the minutes of its latest policy meeting in March, when the FOMC hiked interest rates for the first time since 2018 and said it intends to continue raising rates to a “neutral level that neither stimulates nor slows growth.” “level.

In addition to raising interest rates, the balance sheet reduction is the second pillar of the Fed’s plan to scale back the massive monetary stimulus it injected into the economy at the start of the pandemic.

Robert Rosener, senior U.S. economist at Morgan Stanley, said: “Looking at the balance sheet plans released by the FOMC, it’s hard to feel that they’re not at all serious about unwinding policy easing.”

Here’s what the Fed is proposing and why financial markets are on edge:

How will the Fed shrink its balance sheet?

Officials generally agreed that the Fed should shed as much as $95 billion a month from the central bank’s massive balance sheet and increase to that level in about three months starting in May.

The Fed will seek to “roll over” $60 billion of U.S. Treasuries each month and not reinvest the proceeds of maturing bonds. When the number of maturing U.S. Treasuries falls below that level, the central bank recommends making up the difference by reducing its holdings of short-term Treasuries, which hold about $325 billion worth of short-term Treasuries.

The Fed also wants to reduce its holdings of agency mortgage-backed securities it began buying during the pandemic, limiting monthly reductions in this asset class to $35 billion. However, economists say it may fall short of that target given the securities are expected to mature.

Stephen Stanley, an economist at Amherst Pierpont, estimates that institutional MBS holdings will fall by just $25 billion a month. Fed policymakers have said they will consider selling some of their inventories outright rather than waiting for securities to roll off the balance sheet, but that will only happen if the trimming process “goes well.”

How aggressive is the Fed’s plan?

Soaring inflation plus one of tightest The historical labor market has prompted the Fed to plan to shrink its balance sheet much faster than its last attempt.

After sucking up bonds after the 2008 financial crisis, the Fed waited until 2015 to raise interest rates before shrinking its balance sheet for another two years or so. The Fed then spent about another year raising the asset reduction cap to $50 billion a month.

Fed Governor Lyle Brainard, who is preparing to become vice chair, said this week, fast peace This time is necessary “given that the recovery is much stronger and faster than the previous cycle”.

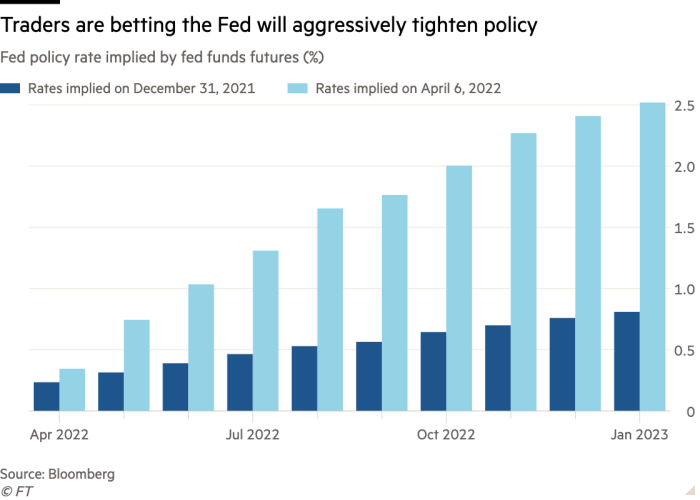

The Fed has taken a similar approach to rate hikes and now has many officials backing Raise rates by half a point at one or more meetings this year — the first time such a rate hike has been used since 2000. Wall Street is bracing for multiple half-point corrections, the first of which was in May.

“By gradually raising the rhetoric, [the Fed has] Diana Amoa, chief investment officer at hedge fund Kirkoswald, said:

How did the financial markets react?

The beginning of the end of the Fed’s pandemic-era stimulus has affected every corner of financial markets. A record rally in U.S. stocks and a housing boom have been built on low borrowing costs brought about by the Federal Reserve’s ultra-easy monetary policy.

Borrowing costs have risen sharply since early March, as mortgage rates surged in anticipation of higher rates, stocks tumbled from record highs. A smaller Fed balance sheet could accelerate these trends.

As the Fed retreats, the supply of Treasuries available to investors will surge, pushing U.S. government bond yields – which rose to three-year highs on Wednesday – higher.

Will there be liquidity issues?

The flood of supply could also have an impact on liquidity (the ease with which traders can buy and sell) in the U.S. Treasury market, which has deteriorated to the point of worst level since the beginning of the pandemic.

“In an environment of heightened volatility and a lot of uncertainty, the market needs to absorb a lot of Treasury collateral,” said Mark Cabana, head of U.S. rates strategy at Bank of America.

the chaos that ensued One last attempt by the Fed to shrink its balance sheet. Short-term funding rates spiked in 2019, signaling that central banks have pulled too much out of the market. However, the Fed hopes it can avoid a repeat of this particular liquidity problem, as it established a permanent facility last year that allows eligible investors to exchange U.S. Treasuries for cash.

[ad_2]

Source link