[ad_1]

This year is set to be a bumper one for bonuses, due to the high profits generated in finance during the past 12 months. But those lucky enough to receive one are weighing the impact of higher taxes, rising inflation and interest rates as they plan to deploy their cash.

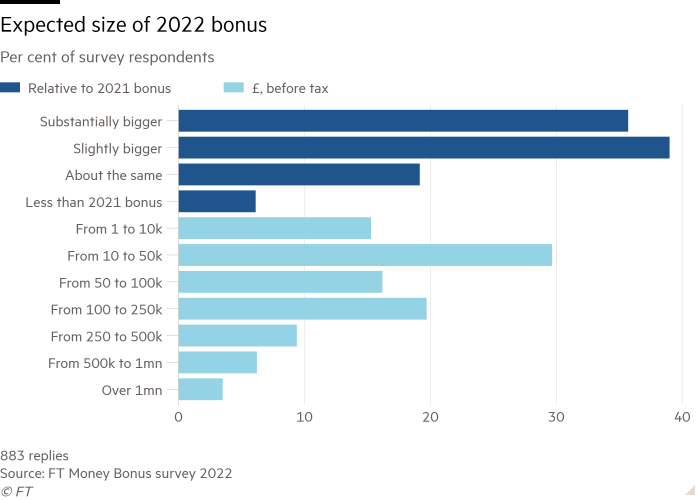

Three-quarters of FT readers say their 2022 bonus will be bigger or substantially bigger than last year’s pay out. Our recent poll of nearly 900 readers found that 40 per cent expected six-figure sums.

One in five readers said their total bonus would be valued between £100,000 and £250,000, and one in three expected to be awarded between £10,000 and £50,000.

We also asked readers whether they intended to invest, spend or save the cash element of their bonus, and why.

“When it comes to bonuses, high earners tend to drift towards two very different extremes,” says Maike Currie, head of personal finance at Fidelity. “They’re either very sensible and invest the lot, or live beyond their means throughout the year, and rely on the bonus money to pay off debts they’ve racked up.”

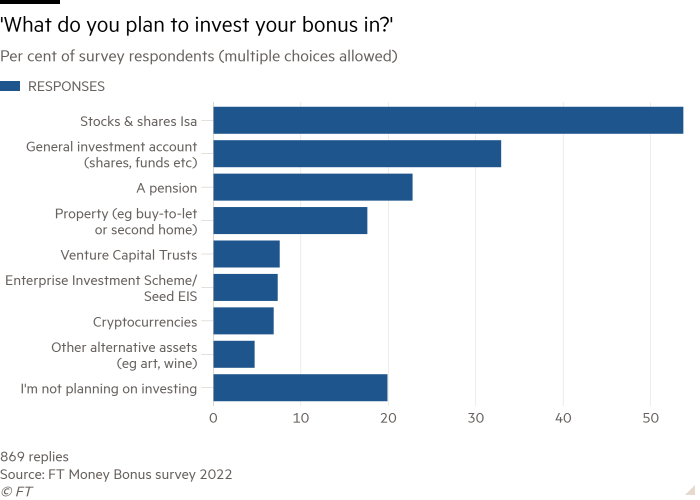

You won’t be surprised to learn that 58 per cent of the FT readers polled said investing the money was their primary aim. More than a third of respondents did not plan to spend a single penny. Most intend to maximise the tax wrappers and allowances detailed below to ensure their money goes as far as possible.

However, rising inflation and interest rates weigh heavily on readers’ minds. Plenty are shifting their investment strategy and the rising cost of borrowing has convinced 13 per cent of readers to pay off a chunk of their mortgage.

Others are taking a different approach to manage inflation, with 11 per cent of readers saying they will spend the majority of their bonus this year.

“If that’s the case, halve what you think you’re going to get in your mind,” Currie advises, noting that tax and national insurance will swallow nearly half of what high earners will take home in cash — more if they’re still repaying student loans.

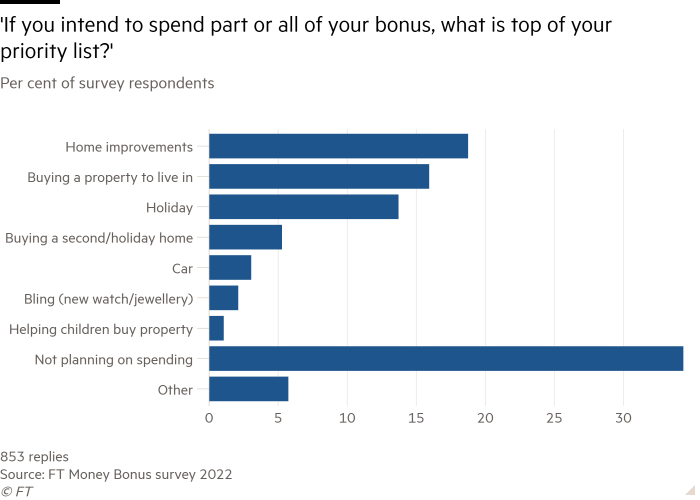

Spending on home improvements was the top answer for readers, closely followed by buying a property or trading up. The next most popular answer was blowing some cash on a foreign holiday as Covid travel restrictions end.

One reader justified this decision as “investing in memory creation” but another was more honest: “I’ve worked my arse off earning my bonus this year, so I’m going to enjoy it. Life’s too short!”

Whether you intend to spend, save or invest any bonus money coming your way, the insights below from readers and experts will help you make the most of the money.

Protecting your bonus from tax

There are plenty of tax advantages for those who choose to invest their bonus, but staying on top of different rules can be taxing.

Income tax

If your bonus is likely to push your total pay over the £100,000 mark for the first time, be aware this could trigger a future tax bill — even if you are a salaried employee. This is due to the gradual withdrawal of the £12,570 personal allowance, which results in a 60 per cent marginal rate of tax on income between £100,000 and £125,140.

Any extra charges won’t necessarily be collected via the PAYE system (this is why HM Revenue & Customs requires everyone earning over £100,000 to complete an annual tax return).

If your employer offers “salary sacrifice” arrangements, you could avoid the hassle of tax returns (and tax charges) by paying more into the company pension scheme, taking your salary below £100,000. These schemes are popular with employers, as they also offer substantial national insurance savings — even more so when NI rates rise in April.

You can also use tax relief on personal pensions (Sipps) to navigate the 60 per cent rate, but you won’t get the NI savings and will need to claim back higher rate relief via your tax return.

The same tactics can be used by those earning more than £150,000, at which point the 45 per cent additional rate of income tax applies.

Pensions

The best protective “tax wrapper” for bonus cash, especially if your employer matches contributions, 23 per cent of readers say they plan to make the most of this — though tax limits are a growing issue.

Many companies offer employees the option of investing all or part of their bonus directly into their pension — up to a limit. Most people have an annual allowance of £40,000 (the combination of employee and employer contributions).

“Those who have maxed out their annual allowance should act fast and see if they can use the ‘carry forward’ rules to use up any remaining allowance from the 2018-19 tax year,” says Nimesh Shah, chief executive of Blick Rothenburg, the accountancy firm.

Carry forward rules apply to the three preceding tax years, so you’ve only got until April 5 to use up any headroom from 2018-19 — or lose it forever. “If you haven’t got your bonus yet, but know it’s coming, you could shove in cash savings now and replenish them later,” is Shah’s tip.

These rules are especially pertinent to very high earners. As a rule of thumb, when your total earnings exceed £200,000 you are potentially in scope of the pensions taper, which whittles down your annual allowance from £40,000 to as little as £4,000.

Being “capped out” of making further pension savings was the second biggest factor influencing readers’ bonus investment decisions, according to our poll.

Even younger readers are conscious of hitting the frozen £1.073mn lifetime allowance in future years, so were prioritising other forms of investment. “As a 38-year-old, I already have £450,000 compounding away in my pension, so it’s foolish to save much more,” said one.

“Don’t forget that you can also set up stakeholder pensions for your spouse and children,” says Shah. Non-earners who don’t pay tax can have up to £2,880 per year invested on their behalf. Topped up with £720 of tax relief, this is immediately boosted to £3,600.

Isas

Tax efficiency, flexible withdrawals and a £20,000 annual allowance made stocks and shares Isas the number one investment choice, with 54 per cent of readers saying this was the destination for some of their bonus.

Once inside the Isa wrapper funds are sheltered from capital gains tax and dividend tax and future withdrawals are exempt from income tax.

In written responses, plenty of readers said they would fill up their spouse’s £20,000 Isa allowance after using their own. Up to £9,000 per year can be saved into Junior Isas (Jisas) for the under 18s. A tax loophole means £20,000 can additionally be saved into a cash Isa for children aged 16-17 and transferred to an adult stocks and shares Isa when they turn 18.

Finally, readers under 40 — or whose children are aged over 18 — could also take advantage of the Lifetime Isa. Up to £4,000 of your Isa allowance can be paid into a Lisa, attracting a 25 per cent bonus. But the complex rules will not suit everyone — the money has to be used for a property purchase or withdrawn after the age of 60.

General investment account

After exhausting the tax limits on pensions and Isas, bonus money can be deployed into a general investment account (GIA) — something that one-third of respondents said they intended to do.

Unlike an Isa, investments in GIAs are liable to capital gains and dividend taxes in future — but don’t forget your tax-free annual allowances (£12,300 for CGT and £2,000 for dividends).

These limits are per person, so you could make investments in your spouse or civil partner’s name to use up their tax allowances.

Shah urges clients to “do the simple stuff first” before looking at riskier tax-efficient investments such as Venture Capital Trusts and Enterprise Investment Schemes, which 7 per cent of readers said they were considering. “Make sure you really consider the investment case — the tax relief should just be a bonus.”

This message is not lost on FT readers. “I’ll fill my Isa, and put the rest in my GIA as I’ve previously invested in sufficient VCTs for my risk appetite,” one commented.

Even so, 7 per cent of readers were happy to risk putting part of their bonus into unregulated cryptocurrencies.

Protecting your bonus from inflation

Inflation was the number one factor influencing readers’ bonus choices this year, cited by more than one in 10 respondents.

For many, high inflation is a driver to invest more or change their investment strategy, although others used it to justify their decision to spend money now.

Mindful of volatile markets and high valuations, some readers said they would lock in the tax benefits of putting bonus money in their Isa or Sipp, but use the “cash park” facility until they were ready to invest.

“I’m waiting for markets to tank, and will then buy blue-chips and sensible investment trusts,” said one. “A likely dip in stock markets is a good opportunity for building up long-term holdings,” reasoned another.

Rather than try to time the market, other readers said they were shifting strategy by moving away from growth stocks and targeting shares with dividend income.

Interactive Investor, the retail funds platform, has seen dividend payers Unilever and Shell top its most-bought shares in January, while increasing numbers of customers are selecting Capital Gearing and Personal Assets, two investment trusts focused on wealth preservation.

Other investors are eschewing bonds as they seek market-beating returns and some FT readers hope that investing in risky but high-growth UK businesses via Venture Capital Trusts and Enterprise Investment Schemes will boost their returns, with these routes favoured by 7 per cent of respondents.

Top 10 factors FT readers say influenced their financial choices

1. High inflation

2. Capped out of pension

3. Tax efficiency

4. End of Covid travel restrictions

5. Saving for first property or trading up

6 Rising interest rates

7 Desire to retire early

8 Home improvements

9 Paying down mortgage

10 Paying school fees

What’s influencing your decisions about whether to spend, save or invest your bonus this year? Share your views in the comments below or email [email protected]

Laith Khalaf, head of investment analysis at AJ Bell, says investors are targeting shares in sectors that are sources of inflation, in particular energy and commodities, as well as luxury goods. He predicts brands with “pricing power” like Burberry could prosper in an inflationary environment by passing on rising costs to consumers — those flush with bonus cash are unlikely to complain.

“The bottom line is, there’s not a lot you can do about inflation, interest rates, or market volatility, but by using tax shelters shrewdly, you can at least hang on to more of your profits rather than paying them over to the taxman,” he adds.

Moving and improving

Property plans were a driving force for readers who said they intended to save or spend most of their bonus money — though many considered sinking cash into their home to be an investment (of sorts).

Nearly one in five (19 per cent) said they were allocating some of their bonus towards home improvements, with some readers citing the challenges of hybrid working as the reason for this.

“My wife wants an extension, so we are getting an extension,” one wrote. “I will enjoy the improvements now, and they will increase my home’s saleability in five years or so,” said another.

In second place was using the bonus to help buy a property, or trade up, chosen by 16 per cent. “I want to buy my first property before interest rates rise further,” one reader confessed.

“High stamp duty means it’s better to improve than move,” was another opinion shared by plenty of other readers.

Paying down debt

Some 13 per cent of readers said that using their bonus to reduce debts was their primary objective, with the vast majority focusing on their mortgages ahead of expected interest rate rises.

“I want to be in the best possible situation when I remortgage in 15 months,” said one. Another reader with a large mortgage said they craved “the guaranteed returns that paying down debt will provide”.

“We are already seeing clients looking to use bonus payments to reduce their mortgages or obtain a better remortgage deal,” says Andrew Montlake, managing director of mortgage broker Coreco.

“Many seek to take advantage of the standard 10 per cent repayment without penalty clauses that exist on most fixed rate mortgages. This has a dual effect of reducing their monthly payments now, but also ensuring that when the time comes to remortgage, they are able to obtain a lower rate as they will fall into a lower loan-to-value banding.”

For example, Montlake says if a buyer purchasing a £600,000 property was able to use their bonus to boost a £100,000 deposit to £150,000, they would be able to slash the best available mortgage interest from 1.84 to 1.59 per cent on a five-year fix.

This would reduce their monthly payments by £262, saving them £15,720 over the initial five-year period.

More cautious readers said they intended to save bonus cash for future expenditure, with school fees scraping into the top 10 of reasons cited.

“Having school fees to pay in the coming years means I can’t risk keeping the money in anything other than my offset mortgage savings account,” said one reader — a method several readers championed.

Some private schools offer the ability for parents to pay up front, known as “advance funding”. “This is worth exploring as it could protect you from hefty inflation on private school fees in the future,” says Catherine Morgan, financial coach and founder of The Money Panel.

Some schools structure this as an investment scheme, as their charitable status enables them to make tax-free returns on investments, which can be passed on to parents in the form of a discount.

Giving to charity

Despite the inflated size of this year’s pay outs, only 39 per cent of readers said they intended to donate to charity.

Those with philanthropic intentions can use Gift Aid to boost their charitable donations, as well as claiming tax relief — another way that readers earning over £100,000 could manage the 60 per cent tax trap, says Shah.

“It’s worth knowing that you can make donations after the end of the tax year, and carry the relief back to the previous tax year, up until the point that you file your tax return,” he says.

[ad_2]

Source link