[ad_1]

This article is an on-site version of our Unhedged newsletter. Sign up here to get the newsletter sent straight to your inbox every weekday

Good morning. Once a month we write about the CPI report. Rules are rules. I think the market is overacting a bit. Think different? Email me: [email protected].

Small changes, big scares

Let’s start at the end of the movie, and work backwards towards the beginning. The ultimate expression of Thursday’s gnarly market response to the CPI report can be seen in the fed funds futures market. Before the report, the futures implied a one in four chance that the central bank would do a double-weight rate increase — half a percentage point — in March. After the report, the probability rose to more than 90 per cent. Oh, the drama:

Broadening the frame, the whole interest rate curve moved up. The two-year bond followed the fed fund futures, pricing in an additional rate increase almost immediately. That’s a whopping big move. While the long end of the curve moved up non-trivially , as well, the flattening of the curve was significant.

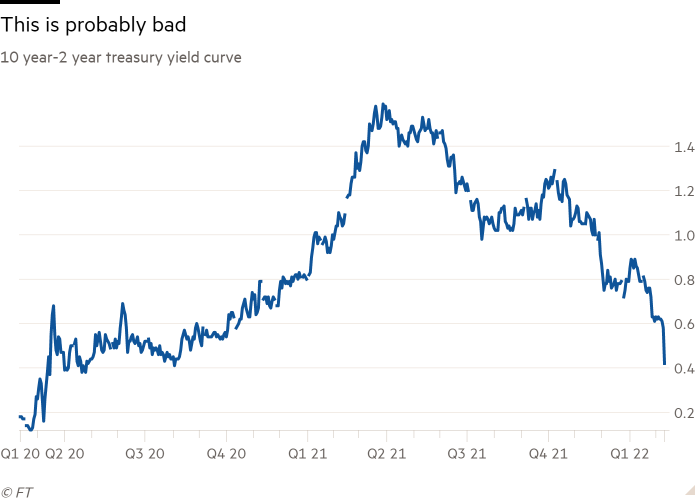

A flatter curve may not make tons of sense, in the abstract, as an indicator that the Fed will tighten policy so abruptly that it causes a recession. But the market, like the heart, has reasons that reason cannot know. Inverted curves scare everyone to death. The 10-year minus 2-year curve has now fallen 1.2 percentage point since March. Another half a point and it’s inverted. Expect to see a lot of pictures like this in the next few weeks:

Fear was perceptible in the stock market, too. The Nasdaq lost more than 2 per cent, as the increase in long-bond yields was driven, once again, by an increase in real yieldsnot inflation expectations (once again: Is there good reason tech stocks need to move conversely with real yields? Not really. Does that seem to be the pattern these days? Sure does).

The S&P didn’t do much better.

Some part of yesterday’s febrile climate is down to James Bullard, who runs the St Louis branch of the Fed. Mid-day yesterday, Bloomberg reported that Bullard supports raising the policy rate to 1 per cent by mid-year. He was also quite flirty about the possibility of a 50 basis point move in March.

But the main culprit was the CPI report itself, of course. Headlines latched on to the year-over-year increase in the full index. At 7.5 per cent, it was at a multi-decade high and perhaps 30 basis points higher than expected . At Unhedged, we’ve lately become converts to looking at the month-to-month core numbers. Here is a picture:

Start with core inflation (that is, excluding food and energy) in dark blue. After two months of deceleration, it was basically flat, which is not great, but north of horrific. Second: durable goods, where inflationary pressure has been greatest, in light blue. It fell a little in January — an encouraging sign. Third: core non-durable goods, in mid-blue. This is clothes, tobacco, cleaning products, and the like. Slowing for the fourth straight month. Good stuff .

Not an awful picture, so far. So why the violent reaction? Rent picked up a bit, but that was widely expected. Was the market looking for more deceleration this month? Certainly, there is a strong consensus that inflation will decline significantly this year , but not until the second half. The wild reaction is a bit of a puzzle.

Here is a possible explanation. Look at the little red bars, above. Services inflation accelerated. Just by a touch; but as I’ve noted a month agoany acceleration looks bad, if you are inclined to think inflation is going to get dug in.

To reiterate. The overarching narrative of the current inflationary incident is that the pandemic makes it hard to consume services, which so often require proximity. The stimulus programmes ensure American households and companies maintain, and in some cases increase, their spending power. Demand shifts massively to goods. Supply chains can’t keep up, and prices rise. If services prices rise, therefore, that is a sign of inflation “leakage” beyond the places where the problem began. And the leakage is bringing inflation to places where prices tend to stick, such as rent and personal services, from haircuts to car repair.

Consider the Atlanta Fed’s index of those historically “sticky” prices (one month changes, annualised):

The January sticky-price increase was the biggest monthly move (4.3 to 7.5 per cent) since the start of the pandemic. And this comes on top of strong moves up in the Fed’s preferred measure of wages, the employment cost indexwhich is now running at a four per cent annual rate in its last quarterly reading (wage increases are thought to be a main channel though which price increases spread).

The CPI report, to sum up, had just enough in it to whip up fears of sticky inflation that were already present in markets. That said, Thursday’s market response looks like an overshoot. The plain fact is that January’s report was only marginally worse than December’s.

Markets are jumpy. Be careful out there.

One good read

You cannot consider yourself a proper inflation geek until you have read a 26-page paper about how nail prices have changed over the last 325 years. I mean, look at this:

Nails!

[ad_2]

Source link