[ad_1]

Once, central bankers knew what they needed to do to deal with inflation. As they struggled to deal with the economic consequences of the coronavirus pandemic, the consensus on how to best promote low and stable price growth has broken.

After years of setting interest rates based on inflation forecasts and seeking to reach a target of about 2%, major monetary authorities around the world are adopting different strategies.

OECD Warning this week “Need to be vigilant”, but any attempt to raise interest rates should “depend on the state and be guided by continuous improvement in the labor market, signs of persistent inflationary pressure, and changes in fiscal policy stance”-so vague that every major The central bank can say that its policies meet the standards.

The Fed has Change position In order to give inflation more leeway and prioritize employment, the European Central Bank has continued to struggle with the issue of whether it can tolerate inflation overshoots, while the Bank of Japan is trying to revive consumer price growth expectations, but to no avail.

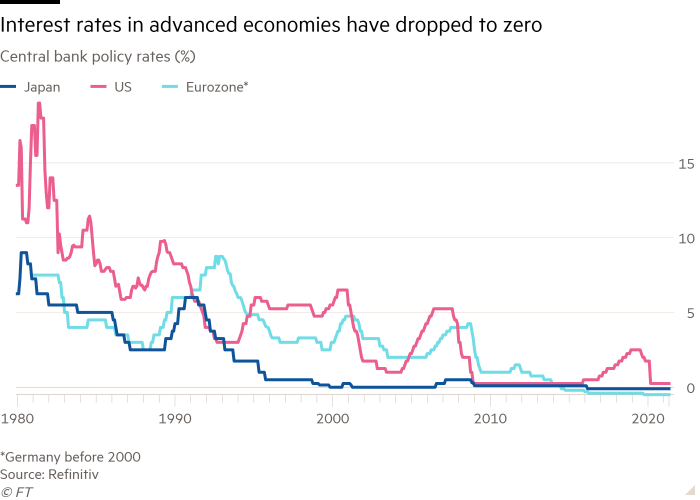

Inflation: a new era?

Prices in many major economies are rising. The British “Financial Times” investigates whether inflation will recover forever.

Day 1: For decades, advanced economies have not faced rapidly rising inflation. Is this going to change?

Day 2: The global consensus among central bankers on how to best promote low and stable inflation has broken.

Day 3: Canaries in the coal mines of American inflation: used cars.

Day 4: How the virus destroys official inflation statistics.

Day 5: Why price increases in developed economies are a problem for debt-laden developing countries.

The strategic shift in the United States is the most radical. Last year, Federal Reserve Chairman Jay Powell announced a new monetary framework.

The Fed’s creed seeks to get rid of decades of preemptive interest rate hikes to avoid potential inflationary pressures, while at the same time more stubbornly pursue full employment. It believes that this strategy will benefit more Americans, including low-wage workers and minorities.

It will allow inflation to be higher than its 2% target for a period of time after it has been below the target for a long period of time to ensure that companies and companies expect interest rates to remain low for a long period of time and therefore spend money instead of saving. One of the Fed’s motivations was to avoid repeating its position after the financial crisis, when policy tightening slowed the recovery.

“I am concerned about the risks on both sides of this expected path,” Lyle Brainard saysOn Tuesday, the Fed governor.She said that she will “carefully monitor” inflation data to ensure that it does not develop in an “unwelcome way”, but will also “be aware of the risk of premature retracement,” and warned that “low equilibrium interest rates” Pre-pandemic trends [and] People with “low underlying trend inflation” may “reiterate” themselves.

But critics worry that the Fed’s strategy is designed for a world of prudent fiscal policy, not for the era of a pandemic. Large amounts of borrowing and spendingIf price pressure increases, this may cause it to fall behind the curve.

The annual growth rate on Friday was 3.1% Core personal consumption expenditure The index reinforces some of these concerns.

For the past five years, the Bank of Japan has been pursuing the promise of inflation overshoot, but it has not even approached its 2% target. Little has changed after the pandemic: Inflation has nowhere to go Coming soon, spending growth is slow.

Japanese households and companies believe that inflation will remain close to zero, making it almost impossible for the Bank of Japan to achieve its goals.

In a recent speech, Bank of Japan Governor Haruhiko Kuroda said: “The formation of Japan’s inflation expectations is not only affected by the observed inflation rate at the time, but also by past experience and norms established in the process.”

At the same time, Eurozone policymakers are involved in a discuss aggressively When the European Central Bank conducts its own policy review; the results will be announced in September.

Oli Rehn, who serves on the Board of Governors as the governor of the Bank of Finland, recently stated: “From an economic and social welfare point of view, it makes sense to accept a certain period of economic growth. [inflation] Overshoot, taking into account the history of overshoot. “

But Isabel Schnabel, the executive director of the European Central Bank, warned that this would be risky.Schnabel said last month that although the central bank should not overreact If inflation exceeds After the delay in action, she was “skeptical” about officially targeting the average inflation rate in a given period.

“How long should the average calculation period be? How much should it be communicated?” she asked. “I personally think we should not follow this strategy.”

For some economists, these differences are irrelevant: monetary policy has become so extensive that central bank governors lack effective tools to take more action.

BNP Paribas Asset Management Corporation Macro Research Manager Chad Barwell said that the European Central Bank has almost “no ammunition”. Although the Eurozone inflation rate in May was slightly higher than its close but below 2% target, it needs to be ambitious. The fiscal policy, or simply taking good luck, can last for a while.

“Unless Europe is about to introduce some large-scale Biden-style fiscal stimulus measures, or the headwind of deflation suddenly dissipates, the monetary stimulus amount needed to raise the inflation rate above 2% is… well beyond their capabilities. ,”He says.

This makes the Fed face difficult choices in the coming months.U.S. inflation is Exceed goal, The demand is strong, it is necessary to decide whether to apply the brake lightly

Policymakers are preparing to start a debate to reduce some of their support, but they show no signs of faltering with the new policy framework, insisting that the recent rise in inflation may be temporary rather than continuous.

Last week, Fed Vice Chairman Randall Quarles stated that the framework is designed for the current world of “slow labor force growth, low potential growth, low potential inflation, and therefore low interest rates”.

“I am not worried about going back to the 1970s,” he said.

[ad_2]

Source link